Market trends

A Closer Look At Luxury Consumption In Asia

From Luxury society

Paurav Shukla

Asia may be an emerging sweet spot for luxury, but consumers in each region have varying value perceptions and buying behaviours, so brands should steer clear of the cookie-cutter approach if they want to truly succeed, explains Paurav Shukla, Professor of Luxury Brand Marketing at Glasgow Caledonian University.

While luxury in Asia is booming with the rise of new money and an affluent consumption class, the picture is not all rosy for the luxury brands within or outside of Asia.

Some remarkable examples of this struggle involve Prada and Mulberry in China, Aigner and De Grisogono in India and Ermenegildo Zegna – entering, leaving, and re-entering the markets. Moreover, with Chinese gift-giving on sudden decline with the subtle messages from its political leadership, many luxury brands have their work cut out for the present and future in figuring out how to succeed in these rapidly growing, but ever so competitive and fickle markets.

In a recent research paper, published in the journal ‘Marketing Letters’, my co-authors – Jaywant Singh (Kingston University, UK) and Madhumita Banerjee (American University of Sharjah, UAE) – and I attempted to decipher the underlying value perceptions that drive luxury consumption among three of the largest emerging Asian economies, namely, China, India and Indonesia.

The following is a presentation of some of our findings, which will discuss how these consumers differ significantly from each other, the underlying problems at hand, and possible ways of engaging luxury customers in each of these markets.

“ Asia can no longer be approached as a laggard market, where consumers will buy anything foreign ”

Why Are Some Companies Struggling In Asia?

I’ll start with the challenges facing luxury brands first. Analysts ascribe the underperformance of some luxury brands in Asia to over-expectations from the market and, particularly, to the treatment of many Asian markets as homogenous.

Asia cannot be approached as a laggard market anymore, where consumers will buy anything just because it’s foreign, or has European heritage.

While business analysts and research scholars emphasise the diversity and uniqueness of individual country markets in terms of geography, demography, culture, and consumption patterns, market realities suggest that many Western luxury businesses might have erred in considering Asia as a homogenous market.

Indeed, many times in our own travels, we have seen the same adverts, the same message and the same communication means employed by luxury brands across Asia to serve these vastly different markets.

This homogenous treatment of Asian consumers baffled us and hence we decided to investigate further and ask some key questions as to:

• What underlying values consumers in Asia associate with luxury brands? And;

• How can a luxury brand profit from these rapidly growing, competitive and diverse markets?

Prada Eyewear, 2014 Campaign

The Framework

We all buy and consume what we believe offers value. Hence, value is one of the fundamental drivers of consumption decisions.

For regularly consumed products, value can be largely derived as a trade-off between costs (mostly price) and benefits (utility). However, in case of luxury goods, this equation becomes significantly more complex as costs are considerably high and, in addition, the benefits are not just utility-oriented but significantly more hedonic in nature at a personal as well as social level.

Using the philosophical framework developed by Berthon et al. (2009) who employed Karl Popper’s “Three Worlds” hypothesis – we examined the constituent value perceptions among Chinese, Indian and Indonesian consumers.

Based on earlier debate, we conceptualised luxury brands with three distinct value-based dimensions:

• Symbolic;

• Experiential, and

• Functional.

The symbolic dimension is reflected in social signals which are constructed through the narrative associated with the brand’s meaning, myth, stories, and consumers’ own wealth, prestige, and social status.

The functional dimension relates to the material embodiment which reflects in physical manifestations, such as quality of material and craftsmanship.

Finally, the experiential dimension is associated with subjectivity and is idiosyncratic, as it differs from person to person. It is reflected through sensations, feelings, cognitions, and behavioural intentions aroused by brand-related stimuli such as logo, packaging, advertisements, and store environment.

Incorporating the instrumental and expressive aspects of the theory of impression management, we extended Berthon et al.’s (2009) three-component model by including two specific sub-dimensions for symbolic value: other-directed symbolism and self-directed symbolism.

We argue that symbolic value is reflected not only through social signals (i.e., instrumental aspect — other-directed symbolism) but also through possessions that help build a unique image for the desired personality (i.e., expressive aspect — self-directed symbolism).

We then asked luxury consumers in India, China and Indonesia about their luxury value perceptions with a sample size of more than 600 luxury consumers and employed structural equation modelling to analyse the results.

“ We asked luxury consumers in India, China and Indonesia about their luxury value perceptions ”

The Breakdown

Indian Consumers

In India, the construct of other-directed symbolism is found to be significantly related to luxury value perceptions, conforming to the crucial role of the instrumental aspect of impression management.

Thus, Indian luxury brand consumers seem to be significantly influenced by what others think of them and, therefore, consume in a way to influence others in order to achieve societal acceptance, reflecting the hierarchical nature of the society (vertical collectivist).

Basically, they use luxury brands most to indicate social status and, more importantly, as a means to symbolise achievement, wealth and prestige.

Indonesian Consumers

Whilst Indian consumers were predominantly influenced by other-directed symbolic value, luxury value perception of Indonesian consumers, on the other hand, is influenced by the self-directed symbolism of luxury brands. Self-directed symbolism resonates with expressive self-presentation, wherein the individual seeks to enhance the self through consumption.

This result, while counterintuitive to the general perception of Indonesia as a collectivistic society, can be explained from the lens of equality perspective (horizontal collectivist). While Indonesian consumers in general would see themselves as similar to others, they will not submit to in-group authority if the consumption choice is distasteful to them.

In comparison, for Indians, luxury goods shopping is not an individual experience. It is rooted in the societal process wherein family and friends go together and the decision is group-related rather than an individual decision – hence, stronger other-directed rather than self-directed symbolism is observed.

“ Indonesian consumers show significant impact of experiential value on their luxury value perceptions ”

Indonesian consumers also show significant impact of experiential value on their luxury value perceptions, which is consistent with the earlier result relating to self-directed symbolism.

Experiential value perceptions represent store-level and personal pleasure derived from the consumption of luxury brands.

In this regard, Indonesian consumers use luxury shopping as a way to forget their problems. The differences in the symbolic value perceptions between Indian and Indonesian customers are also consistent with what is observed in prior literature which shows that social and self-directed behaviour vary as per cultural differences.

Chinese Consumers

Functional value perception, in particular, has a significant impact on luxury value perceptions among Chinese consumers.

However, as a value perception this was significant across all three countries in the study. This result shows that consumers evaluate the functional value of a luxury brand in terms of the status it brings and therefore are willing to pay a premium price.

The three countries have witnessed rapid economic growth over the last two decades and a consequential increase in aspirational consumers. These consumers associate prestige through the price and product quality perceptions and therefore buy luxury brands, which are perceived to accord higher status in the eyes of their societies.

How To Customise Your Luxury Strategy In Asia

Marketers can benefit from knowledge about the differences (and similarities) in constituent luxury value perceptions and customise or standardise their marketing strategy accordingly.

For instance, a luxury brand positioning strategy in Indonesia should emphasise how the brand could enhance a consumer’s self-image and could make them feel good about themselves, as well as focus on the experiential aspects of buying and using the brand. Moreover, a brand will have to offer a unique store-level experience to Indonesians.

On the other hand, a luxury brand in India should focus more on how the brand could add to the buyers’ social status.

Marketing a luxury brand to Indian consumers by stating its European heritage and highlighting foreign origin may not work as these consumers are well-travelled and aware of global trends.

Moreover, they have a strong Indian luxury heritage connection, so a luxury brand which wants to establish itself in the Indian market will have to work on social acceptability and symbolism of achievement, prestige and wealth.

This wealth connection is also integrated with functional value, as Indian consumers associate higher price with higher quality and desire products that are harder to get.

The higher price and social symbolism also adds significant meaning to a luxury brand for Chinese consumers also.

Thus, overall, the results gathered to date suggest that luxury brand marketers should customise their positioning and communication strategies for symbolic and experiential value perceptions across the three countries.

Given that functional value has a significant impact on luxury value perceptions in all three countries, marketers could achieve scale economies by standardising their strategy for this dimension of luxury value perception.

Reference: Shukla, Paurav, Jaywant Singh, Madhumita Banerjee (2015), “They are Not All Same: Variations in Asian Consumers’ Value Perceptions of Luxury Brands,” Marketing Letters, Forthcoming.

Additional editing by Daniela Aroche, Editorial Director of Luxury Society

2016 - Retail trends & predictions

Welcome to Vend’s 2016 Retail Trends and Predictions report – a collection of our top 12 forecasts for the retail industry. Just like our 2015 predictions, this year’s forecasts will shed light on the trends and issues that’ll make (or continue to make) a big impact on the retail industry.

Modern Trade vs traditionnal trade : wolrwide overview

Retailers with international ambitions need to adapt to local needs

Internationalisation among retail occupiers is anything but a new phenomenon. The likes of H&M and Zara are common sights on high streets the world over, while IKEA sheds are an equally omnipresent force out-oftown. However, global retail markets are anything but homogeneous, and the path to international growth is not necessarily paved with gold. Many retailers have successfully made the global transition, others are just starting out in their endeavours. Some retailers are still licking their wounds in the wake of ill-advised or poorly executed overseas forays.

The rewards of successful internationalisation are substantial, but the risks are also manifold. Real estate markets play a fundamental role in the globalisation process and are often the tipping point between success and failure.

To continue to read the report, download it.

Digical® retail and why stores matter - Report from Bain & Company

Moderate growth in November led by digital sales

Bain estimates that the combined growth of in-store and e-commerce retail sales for November hit 3%, with online sales growing at mid-double-digit rates:1

- Early data from the US Census Bureau suggest that November in-store sales increased 1.8% over November 2014. The Census Bureau reported strong results (4% to 5% year over year) for home and home improvement and sporting goods and hobby retailers, and negative growth for both electronics and clothing retailers. Consumers continued to shift spending to nontraditional retail categories—cars and eating out—a trend that is weakening, though, as we get deeper into the holiday season. Year-over-year growth for motor vehicle and parts dealers was 4.3% in November vs. 6.5% in October. Similarly, sales at restaurants grew by 5.4% in November vs. 7.6% in October relative to last year.

- MasterCard estimates that total e-commerce sales in November increased by 16% over the same period last year. Cyber Monday in particular saw a record-breaking $3 billion in revenue—driven in large part by growth in mobile sales of more than 50%. Mobile sales, including purchases using smartphones and tablets, accounted for more than a quarter of e-commerce sales on Cyber Monday, up from 20% last year. It’s important to note, though, that Cyber Monday fell on December 1 in 2014; it fell on November 30 this year. So year-over-year growth estimates for November inclusive of Cyber Monday 2014 are closer to 12%.

Holiday shopping tracker results: Shoppers are two-thirds of the way there

This year, Bain has partnered with Vision Critical to follow a panel of consumers as they shop for the holidays.2 Our panelists are making progress on their lists: Most completed an additional 20% of their shopping in the two weeks following Black Friday and are now two-thirds of the way there (see Figure 1). Our "online fanatics" continue to lead the charge, with more than 30% having completed all of their holiday buying. While our "sticklers for stores" made the most progress over the five-day Thanksgiving weekend, to date only 20% report that they’ve completed their shopping, and almost 15% have yet to start. Research suggests consumers are delaying their holiday shopping this year relative to previous years. Of those who still need to complete their shopping, 20% are holding out for last-minute discounts.

Consumers spend more online during the holidays than they do the rest of the year. Last year, online penetration averaged 10% of all retail sales from January through October, and 12% during November and December. Our Vision Critical panelists confirm this shopping behavior. Both "sticklers for stores" and "omnichannel shoppers" have done a greater percentage of their shopping online this holiday season than they typically do in non-holiday periods. "Online fanatics" continue to make more than 80% of their purchases online.

Stores remain in the spotlight this holiday season

Although online penetration spikes during the holiday season, the reality is that nearly 90% of retail sales still happen in stores. This year, Bain worked with Foursquare to understand how retail foot traffic changes during the holiday months.3 Our findings indicate that consumers go to stores more during the holidays, particularly in the two weeks leading up to Christmas Day

To continue to read this article then click

To download the full article in pdf.

The 2014 Global Retail Development Index™

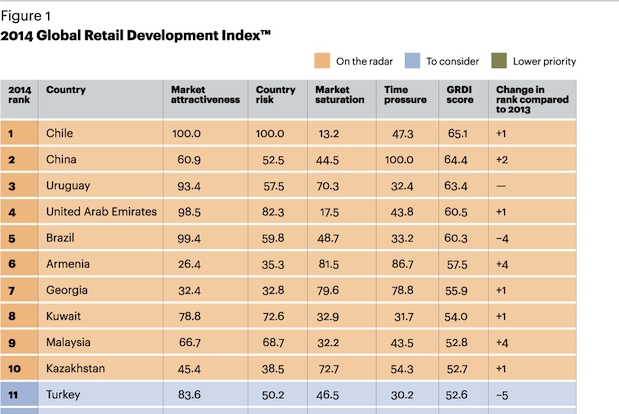

You, as a retailer, you want to develop your brand abroad. The question is to know where to expand your business, in what region of the world. Atkearney, a leading global management consulting firm publish a yearly report regarding the retail industry. In this report countries are ranked depending 4 items:

- market attractiveness

- country risk

- market saturation

- time pressure.

The Global Retail Development Index™ is an annual study that ranks the top 30 developing countries for retail expansion worldwide. The Index analyzes 25 macroeconomic and retail-specific variables to help retailers devise successful global strategies and to identify developing market investment opportunities. The GRDI is unique because it identifies today's most successful markets and those that offer the most potential for the future.

The highlights of the 2014 GRDI include:

- Chile ranks first for the first time. Years of economic and political stability have helped the country build one of South America's most sophisticated retail environments. The past year brought several major investments in malls, new entries by international retailers, and expansions by local leaders.

- China moves back into second place this year. Even as the economy slows and conditions become more difficult for foreign retailers, the huge and growing market is impossible to ignore.

- Sub-Saharan Africa continues to show momentum with three ranked countries, including newcomer Nigeria. GDP growth of 5 percent, rising household incomes, fast urbanization, and a growing middle class give this region massive retail potential.

- Regional players are flexing their muscles, using their proximity as a competitive advantage to steal share in neighboring markets. Chile’s Falabella and Cencosud have begun aggressive growth plans to widen their footprint across Latin America, and UAE-based LuLu Hypermarkets and Majid Al Futtaim have begun expanding in the Gulf region. South African retailers Shoprite and Woolworths have spearheaded Sub-Saharan Africa’s shift to modern retail.

See the report (clik to the link below):